Elvis Torres Delgado

Elvis Torres Delgado Xavier Diví

Xavier Diví

Main Highlights:

• The banking sector reached a Pre-Tax ROE of 20.01% in the first nine months of 2024 on an annualized basis, in line with the 2023 profitability (20.60%). This is the fourth consecutive year with Pre-Tax ROE above 20%. In the previous 20 years, only in 2004 did the banking industry profitability reach above 20% levels.

• Measured on a return on assets basis (before taxes), Oriental Bank and FirstBank showed very high profitability levels (2.25% and 2.11%, respectively), significantly above the US peers average (1.44%). These banks achieved healthy efficiency levels in 2024 and in 2023 with Cost to Income ratios just north of 50%.

• The large public deposits portfolio, which has to be invested in liquid assets, explains, in part, the different asset composition of Banco Popular compared to Oriental Bank and FirstBank. The loan portfolio represented 45% of total assets for Banco Popular in 2024 compared to 68% for Oriental Bank and 66% for FirstBank.

• The banking sector continued to be very well capitalized with the Tier 1 Risk Based Capital Ratio at 15.9% in the Jan-Sep 2024 period. Banks are likely to continue returning capital to shareholders through share buy backs and dividends.

• Loan delinquency remained at historically low levels. The Non-Performing Loans Ratio was 1.73% in 2024, the second lowest in the past 25 years (1.63% in 2004).

• Loan balances grew by 5.2% in the first nine months of 2024 on an annual basis, below the 8.2% increase achieved in 2023. The commercial (CRE +6.0% and C&I +5.7%) and auto (+7.5%) businesses drove the loan portfolio increase, together with the mortgage (+3.5%) and credit card (+3.1%) businesses which showed more modest increases. The personal unsecured portfolio remained slightly above the 2023 level (+1.1%).

Mortgage Business Trends

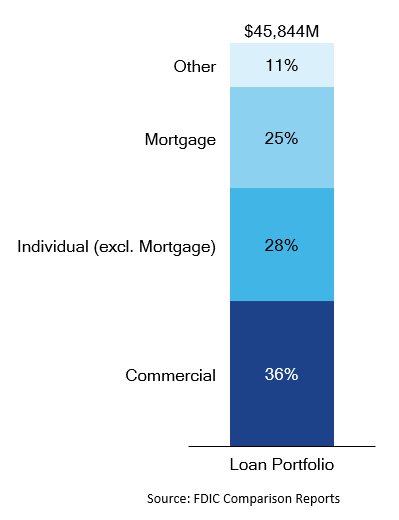

The mortgage portfolio represents 25% of the total lending business for the banking industry in Puerto Rico (see Figure 1). Excluding lending for commercial clients, the mortgage loan portfolio is, by far, the largest for Puerto Rico banks compared to the auto or consumer lending businesses.

Figure 1: PR Banking Industry Loan Portfolio 2024 (Million USD)

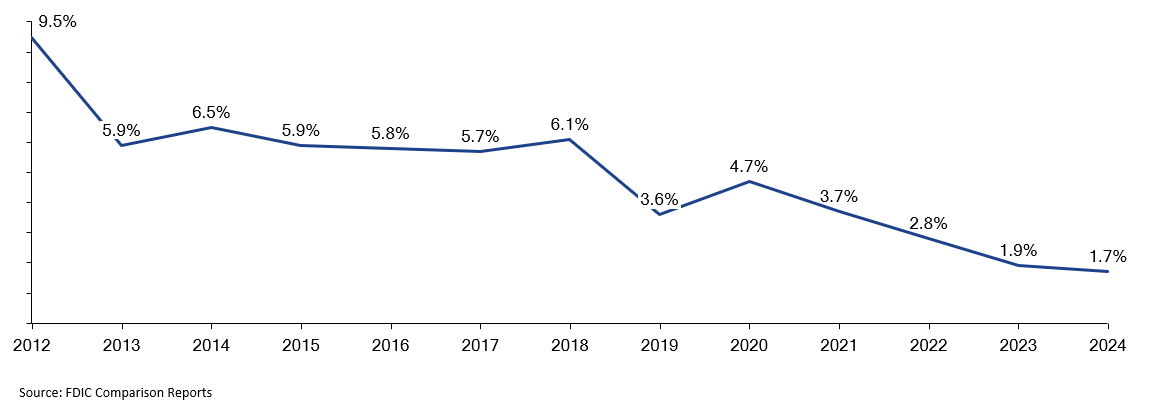

In addition to the size of the mortgage portfolio, the profitability of the mortgage loans owned by banks has improved significantly, driven by the sound credit policies implemented since the 2007-2008 financial crisis and the improvement in the economic landscape. As can be observed in Figure 2, the non-performing mortgage loan base as a percentage of the total mortgage portfolio has reduced quite consistently since 2012. In 2012, the mortgage non-performing loans ratio was 9.5%, almost six times higher than in 2024, when it reached a historical low of 1.7%.

Figure 2: Non-Performing Loans Ratio of Mortgage Portfolio

Given the importance of the mortgage business for local banks and its improved profitability, it is fair to ask ourselves which banks have been able to grow their mortgage portfolios in the past years. It is important to mention that we are not looking at other mortgage operations like mortgage servicing or the business of buying/originating and selling mortgage loans in the secondary market.

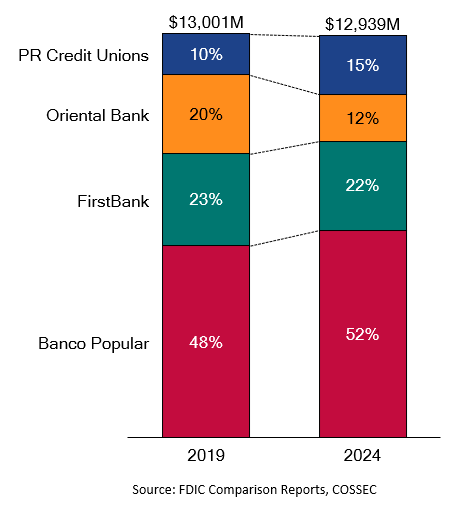

Looking at Figure 3, we can see how the total mortgage portfolio in Puerto Rico has remained stable when we compare 2024 to 2019. The Credit Unions sector in Puerto Rico has been able to increase its mortgage portfolio by about 50% in the period. This sector has managed to leverage its member base, particularly in geographies and demographic profiles that banks struggle to reach, to provide a more personalized service, and to cross sell lending products like mortgage loans. Some 69 credit unions in Puerto Rico also benefitted from the allocation of $226 Million by the U.S. Department of the Treasury in April 2023 to expand their capacity to respond to community development needs like housing.

When looking at banks, Banco Popular showed the largest portfolio growth with its market share increasing from 48% to 52%. Based on Banco Popular’s earning calls, its mortgage portfolio growth is driven, in part, by a strategy to hold on the FHA insured mortgage loans instead of selling them in the secondary market. FirstBank has been able to hold its market share with just a slight decrease from 23% to 22%, while Oriental has suffered an important reduction in its mortgage portfolio since the acquisition of Scotiabank.

Figure 3: Mortgage Loan Portfolio (Million USD)

In order to grow the mortgage loan portfolio, banks may originate loans themselves or purchase them to mortgage companies which do not usually hold loans on a long-term basis in their asset base.

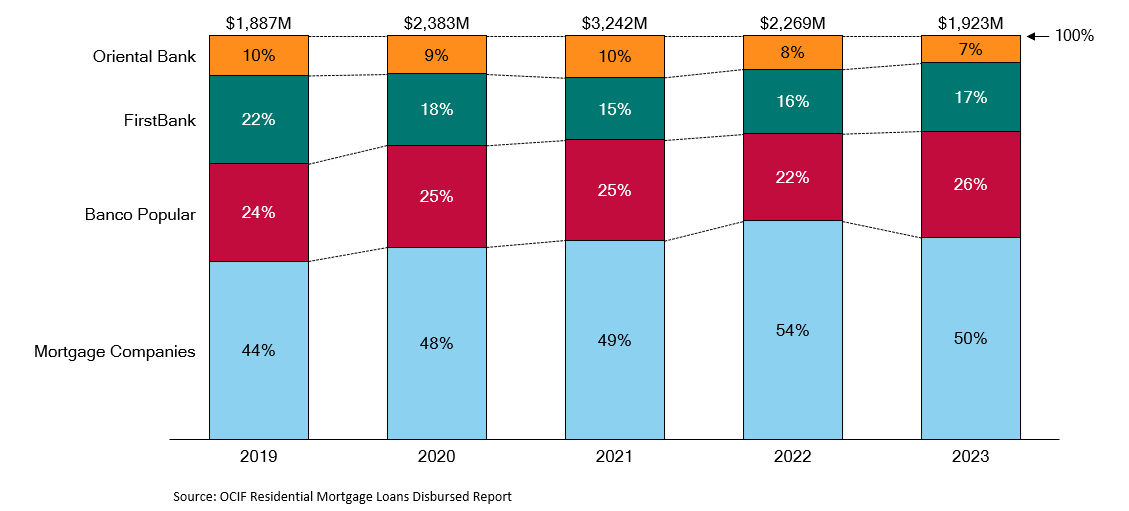

The Puerto Rico economic crisis that started in 2006 translated into a steep reduction in mortgage loan originations. Mortgage originations reduced from $5.1 Billion in 2012 to $1.8 Billion on average in the 2017-19 period. The low-interest rate environment and the Covid 19 relief funds spurred an increase in mortgage originations, both for home purchasing and for refinancing, which reached $3.2 Billion in 2021. The subsequent interest rate increases implemented by the Federal Reserve reduced originations back to the $1.9 Billion level in 2023 (most recent data point available with bank vs mortgage companies split). The overall mortgage originations reduction during the 2012-23 period was mainly suffered by banks when compared to mortgage companies. Mortgage companies increased their share from 26% in 2012 to 50% in 2023 while the banks’ share reduced from 74% to 50% in that period.

Figure 4: Mortgage Originations Banks vs Mortgage Companies 2012-2023 (Billion USD)

When looking at banks during the most recent years, all suffered a market share reduction between 2019 and 2022 (6 percentage points FirstBank and 2 percentage points Oriental Bank and Banco Popular). However, both FirstBank and Banco Popular were able to regain market share in 2023, mainly to the expense of mortgage companies. Particularly noticeable was the ability of Banco Popular to increase mortgage loan originations by 3.6% in 2023 when total originations reduced by 15%.

Figure 5: Mortgage Originations by Mortgage Companies and by Bank 2019-2023 (Billion USD)

In summary, the mortgage lending business is one of great importance for local banks particularly at a time when credit policies are more robust than years ago, and delinquency levels are very low. As banks have plenty of liquidity available to fund their lending businesses, we should see increasing competition to gain mortgage origination and portfolio share particularly if the recent rate cuts drive an increase in the home purchasing and refinancing.

For more information on our economic dashboards please write to xavierdivi@v2aconsulting.com or visit www.v2aconsulting.com.