Opening Remarks

Much has transpired since Hurricanes Irma and Maria swept through Puerto Rico 18 months ago resulting in over $80 billion in damages and more than $25 billion in lost output, decimating the Island”s vulnerable electric grid and other critical infrastructure systems, disrupting normal economic and social life, inducing tens of thousands of Puerto Ricans to flee the Island.

While the progress made should not be understated, given the noble, and at times heroic, work of those individuals and organizations (public and private) committed to the Island”s recovery and reconstruction, the pace of the process has been painstakingly slow and the impact of the incoming Federal funds on the local economy has been limited. Many saw the billions of dollars in post-disaster relief funds flowing into the Island as a silver lining and as a source of a much-needed boost in economic activity. However, the pace of disbursements has been slow and, consequently, the impact on the local economy has been limited thus far. Furthermore, as commonly occurs in post-disaster efforts, nonlocal entities, mostly US mainland contractors, have greatly benefited from the inflow of billions of dollars for disaster recovery and reconstruction, while local contractors have been awarded a small fraction of contracts.

Notwithstanding the setbacks, there are numerous achievements that should be highlighted, especially when considering Puerto Rico”s challenging pre-hurricane context, fiscal woes, and the more than decadelong economic slump. This third V2A post-hurricane issue, at the one-and-a-half year mark of the historic 2017 hurricane season, presents an update on the performance of key macroeconomic indicators following the hurricanes, an analysis of core economic sectors, and a review of past and future disaster relief funding activities.

Post-Disaster Macroeconomic Performance

Economic Activity Index (EAI)

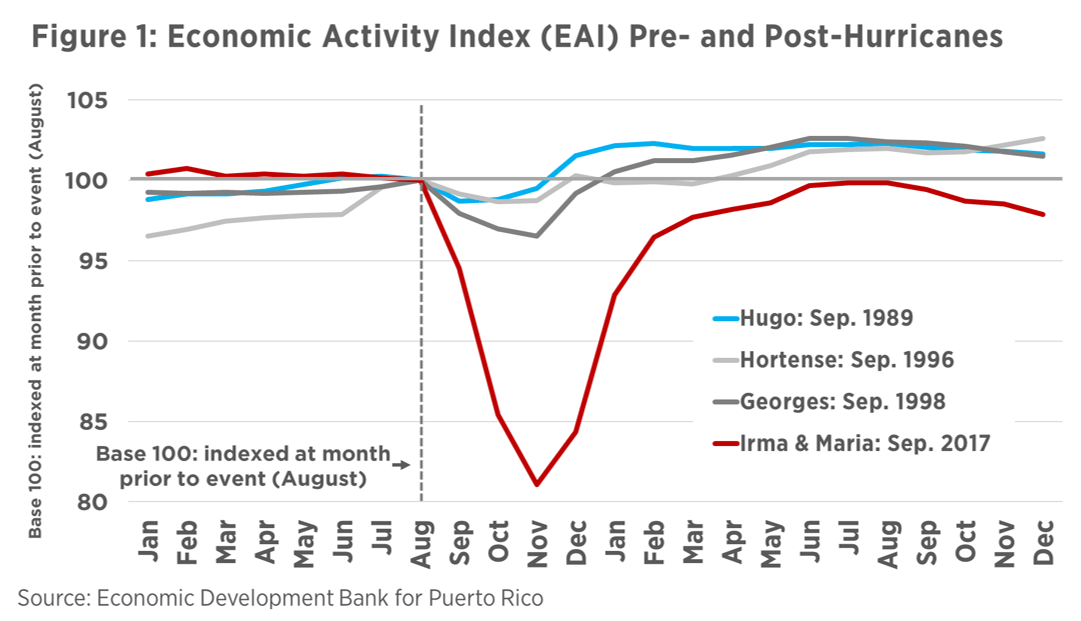

To ascertain and compare the economic progress made following the impact of major hurricane events on the Island, Fig. 1 indexes the Economic Activity Index (EAI)1 to a base of 100 in August, month prior to major tropical cyclones that have impacted Puerto Rico (Hugo in September 1989, Hortense in September 1996, Georges in September 1998 and Irma and Maria in September 2017). It helps to illustrate three key points: first of all, the magnitude of the impact of Irma and Maria on economic activity dwarfs that of previous hurricanes. Puerto Rico”s EAI plummeted in the wake of the hurricanes Irma and Maria, contracting by 14% from August 2017, month prior to the hurricanes, to November 2017, two months after the natural events. Secondly, from this low point, the EAI following Irma and Maria gradually converged to pre-hurricane levels by June 2018, 9 months after impact. In contrast, by December following Hugo in September 1989, Hortense in September 1996 and Georges in September 1998, the EAI had returned to or had surpassed August, pre-hurricane levels. Thirdly, a concerning downward trend is visible after August 2018 with the EAI contracting once again. If the projected private and public disaster relief funding and rollout stated in the latest Fiscal Plan fully materialize ($5.8 billion in FY2019, $8.7 billion in FY2020, and so forth), it will materially stimulate economic activity in the years ahead.

Labor Market Dynamics

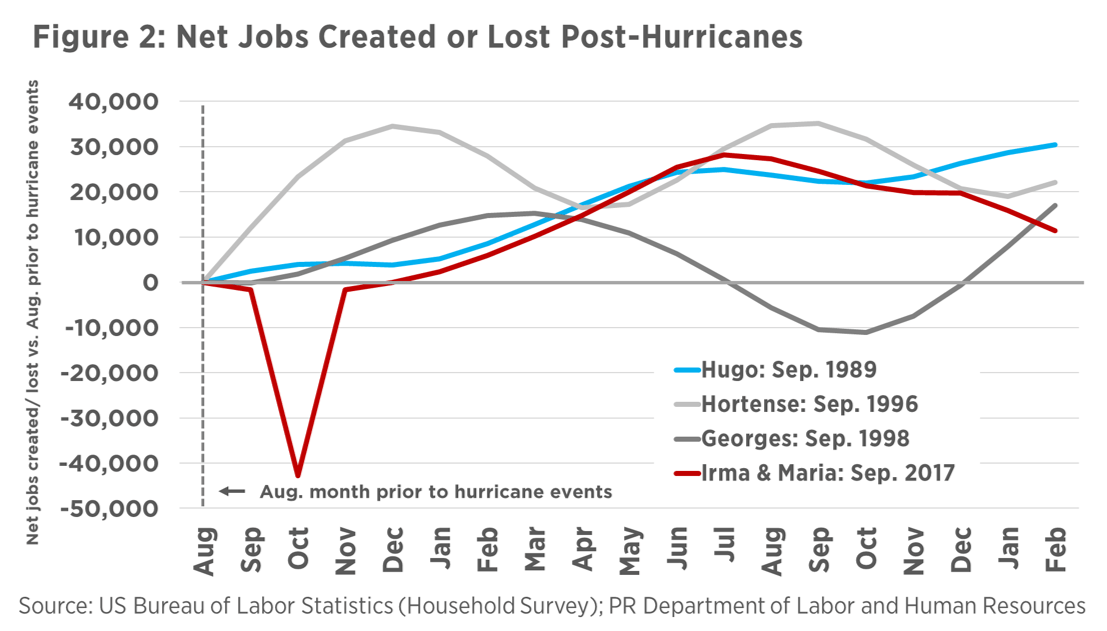

When analyzing post-hurricane labor market indicators, there are mixed results, with the unemployment rate reaching a historic low of 8.5% in February 2019 from being in the double-digits prior to April 2018, while other labor statistics remain stubbornly weak and have been moving in the wrong direction. The labor force participation in February 2019 stood at 40.1%, compared to 63.2% in the US. Furthermore, while total employment (household survey) increased by roughly 28,000 from August 2017 to July 2018, it has been steadily decreasing since, narrowing down the difference between August and February 2019 to 11,400 (see Fig. 2).

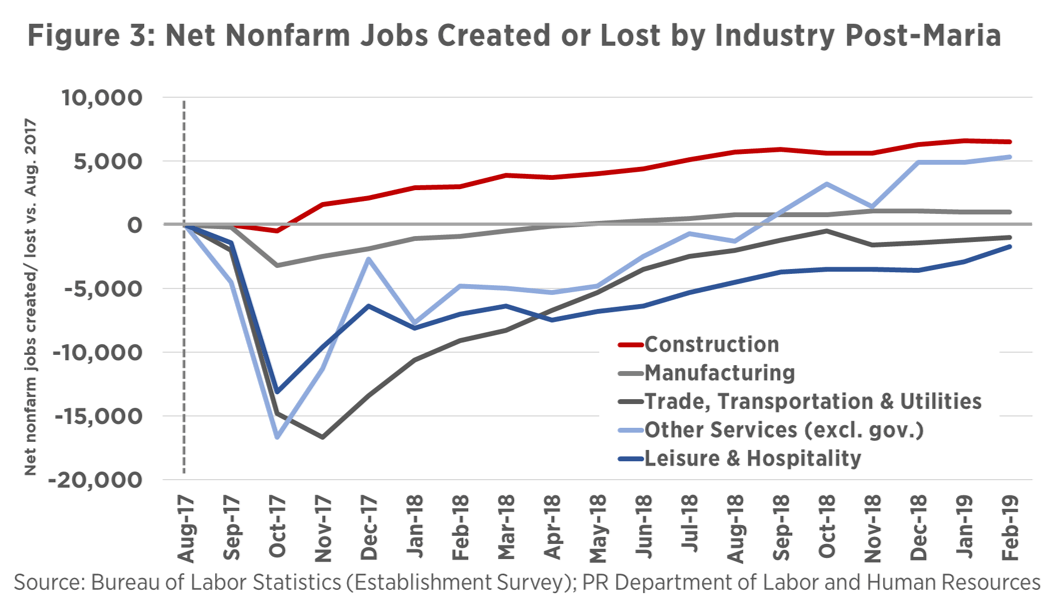

Total employment (establishment survey), excluding the self-employed and agricultural workers, as of February 2019, remained 3,400 jobs below pre-hurricane levels. As seen in Fig. 3, only construction jobs, which reached 27,700 in February 2019 from 21,200 in August 2017, representing an increase of 6,500 jobs or 31%, have shown a material improvement with respect to pre-hurricane levels. Employment in all other industries have either narrowly surpassed pre-hurricane levels or are still below. While tourism activity has shown some signs of improvement, leisure and hospitality employment, as of February 2019, is 1,700 jobs or 2% below August 2017.2

Key Economic Sectors

Housing and Construction Activity

Even prior to Maria, the housing and construction sectors were severely impacted by the protracted economic downturn. Loss of Island-wide real estate equity values has reached close to $30 billion since the onset of the economic downturn. Public and private investment in construction as a percent of real gross national product (GNP) averaged 14% from FY2000 to FY2005, plunging to below 5% after FY2015, 4.5% in FY2016 and 4.1% in FY2017. In nominal terms, construction investment decreased from an average of $6.6 billion from FY2000 to FY2005, to $2.4 billion in FY2017. Furthermore, of the 1.5 million residences in Puerto Rico, roughly 18% were vacant prior to the hurricanes. The local real estate market has also seen a continued drop in home prices and rise in foreclosures.3

The impacts of Irma and Maria exacerbated the precarious state of the housing market. Some 527,000 homeowners reported some degree of damage to their property. FEMA reported that more than 1.06 million households (88% of total), applied for individual disaster assistance. As per the local government”s Disaster Recovery Action Plan4, the full extent of the housing impact caused by Hurricane Maria was estimated to be approximately $33.9 billion.

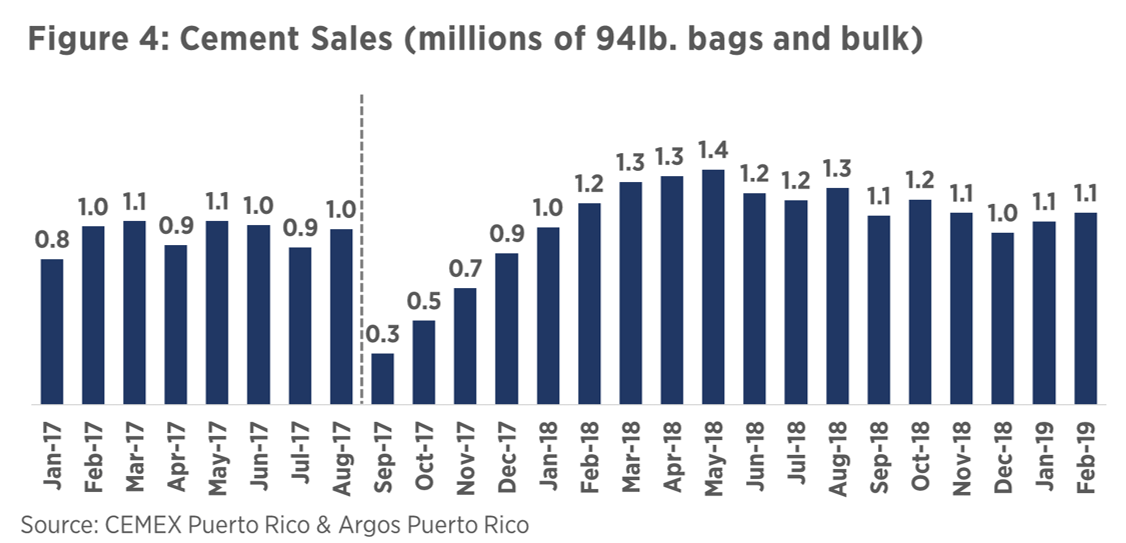

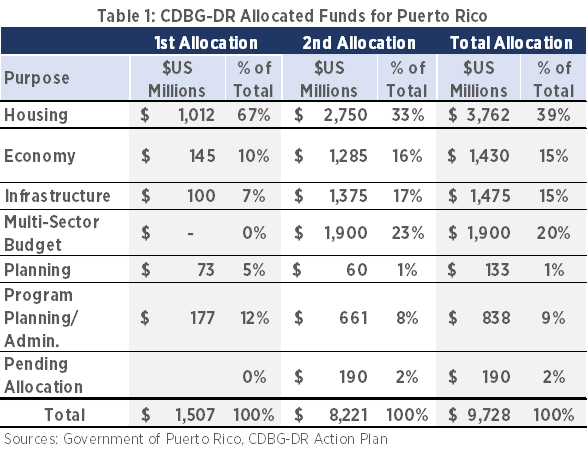

Many anticipated a marked and sustained increase in construction activity in the wake of hurricanes Irma and Maria, driven by billions of dollars in post-disaster reconstruction funds derived from Federal sources and private insurers. After 18 months since September 2017, these expectations have fallen short. As is clearly seen in Figure 4, cement sales, a proxy for construction activity, dropped significantly in the immediate aftermath of the hurricanes, peaked in May 2018 with 1.4 million bags and bulk of cement sold, and quickly returned to the pre-hurricane depressed levels. Of the first allocation through the Community Development Block Grant – Disaster Recovery (CDBG-DR) Program of $1.5 billion, $1 billion were allocated for housing programs, primarily for home repair, reconstruction, or relocation ($776 million). The second allocation of $8.2 billion dollars will direct $3.8 billion for housing ($2.2 billion for home repair, reconstruction, or relocation).

Tourism and the Visitor Economy

Tourism, which represents approximately 6% of Puerto Rico”s economy5, has seen mixed results since the hurricanes significantly impacted the sector. According to the Government of Puerto Rico”s report Transformation and Innovation in the Wake of Devastation: An Economic and Disaster Recovery Plan for Puerto Rico, the tourism sector lost $547 million in direct revenue. Roughly 4,000 hotel rooms of the 15,000 available in Puerto Rico (27%), closed for renovations following Maria. Furthermore, according to a World Travel & Tourism Council Report6 the 2017 hurricane season caused a loss of 826,100 visitors to the Caribbean and $741 million in visitor expenditures.

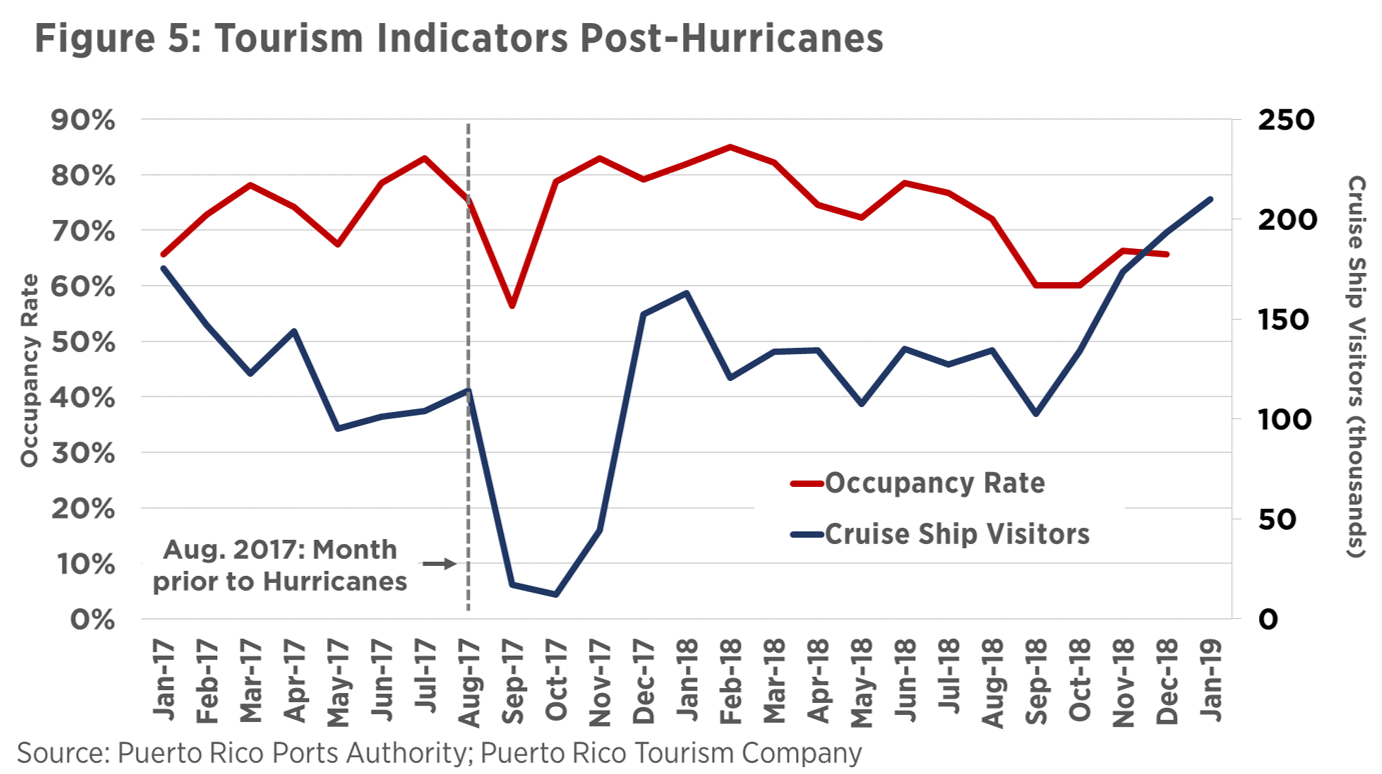

The inflow of first responders to carry out recovery and reconstruction efforts in the wake of the hurricanes materially impacted tourism indicators, particularly the Island”s occupancy rate as can be seen in Figure 5. During the six months following the hurricanes, from October 2017 to March 2018, the occupancy rate averaged 82% and reached 85% in February 2018, one of the highest levels recorded. However, occupancy has been decreasing since, averaging 63% in the last 4 months of 2018. Short-term rentals are increasingly becoming an important player in the local tourism industry, with short-term rental activity increasing from a monthly average of 17,000 room nights booked in 2015 to a monthly average of 109,000 and 149,000 in 2017 and 2018, respectively.7

On a bright note, the cruise ship industry has undergone a marked surge in activity following Irma and Maria, as illustrated in Figure 5. Right after the storms, as expected, cruise ship passenger movement halted almost completely, but quickly rebounded back to pre-hurricane levels and has more recently reached historic highs. During the last three months of available data (November 2018 to January 2019), cruise ship visitors averaged 192,000, recording a historic peak of 210,000 in January 2019. The government hopes to increase the number of cruise ship passengers from 1.4 million to 2 million in 5 to 10 years. Air passenger movement has also recovered post-Maria.8

When it comes to employment in the sector, the latest nonfarm employment report shows that leisure and hospitality jobs reached 78,800 in February 2019 (9% of total nonfarm employment), just 1,700 jobs below the 80,500 reported in August 2017 just prior to the hurricanes.

The World Travel & Tourism Council estimated that recovery in tourism in the Caribbean could take 4 years, missing out on $3 billion in the process.6 One of the key strategic initiatives of the government of Puerto Rico through the newly created Destination Marketing Organization (DMO) whose official name is Discover Puerto Rico, seeks to “develop a strong visitor economy to help position Puerto Rico as a global destination of investment, production, and wealth.”9

Retail and Commercial Activity

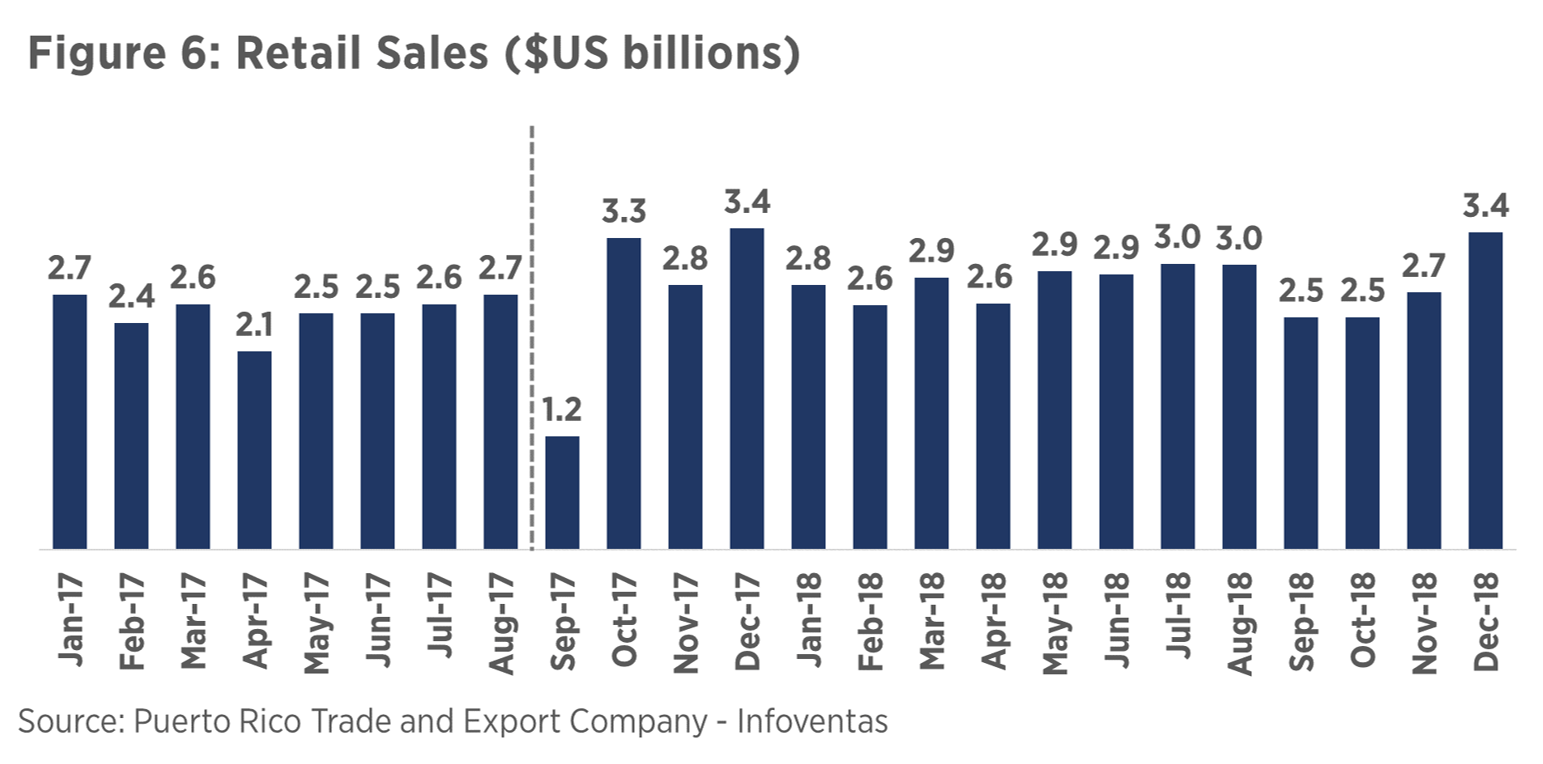

According to the United Retailers Association, close to 8,000 small businesses, 10% of the total, remained closed 1 year after the hurricanes.10 Due to the widespread leveling of critical infrastructure and lifeline systems giving rise to a cash only economy, retail activity in the immediate aftermath of the hurricanes took a nosedive. However, it bounced back rapidly as seen in Figure 6. Consumer confidence has picked up as reflected by retail and auto sales.

Total retail sales reached $33.8 billion in 2018, an increase of $4.4 billion or 14.8% with respect to 2017 ($29.5 billion), driven by Federal fund transfers, disbursement of post-disaster insurance claims and other rebuilding and reconstruction expenditures. Elevated net outmigration and resulting suppressed domestic demand continues to be a downside risk for retail sales going forward. Personal loan originations also provide evidence of the relatively strong performance of consumption activity with personal / consumption loan originations reaching close to $2 billion in 2018, increasing by 16.3% with respect to 2017 and accounting for 30% of all loan originations (13% in 2005).11

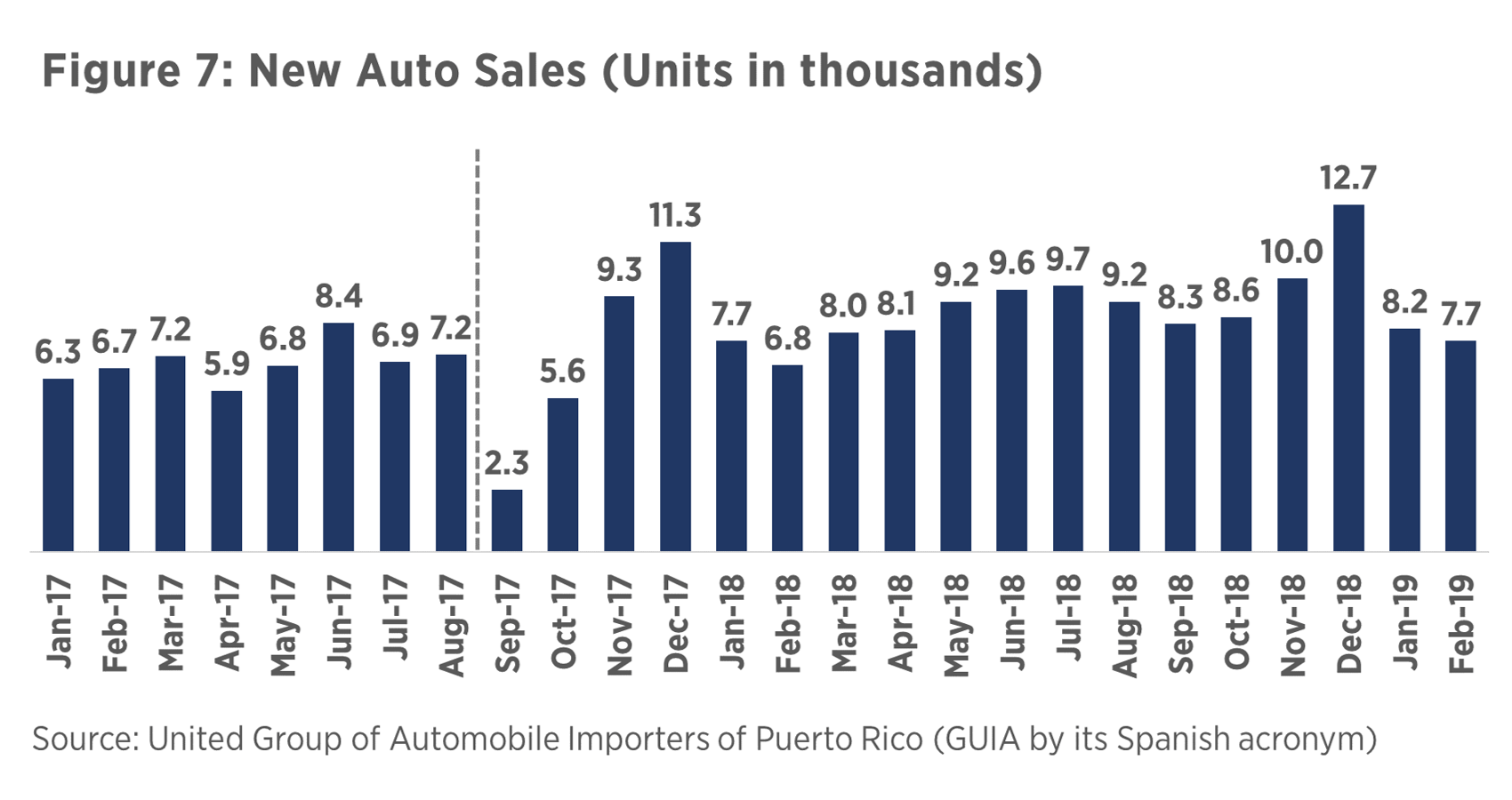

Auto sales also recorded an increase in 2018, growing from 84,080 in 2017 to 107,941 in 2018, an increase of 23,861 units or 28.4% and the first year exceeding the threshold of 100,000 units sold since 2013. Post-hurricane auto insurance claims played an important role in this spike. It should be noted that an important development took place in 2018, with the acquisition of Reliable (Wells Fargo auto finance business) by Popular, making the Island”s largest bank the leader of the auto financing sector with a 49% auto loan market share and a 69% share in auto leasing.12 The auto industry is projecting auto sales to be nearing 90,000 due to the slow disbursement of Federal disaster funds, loss of population, and the still lingering economic weaknesses.13

Banking and Financial Activity

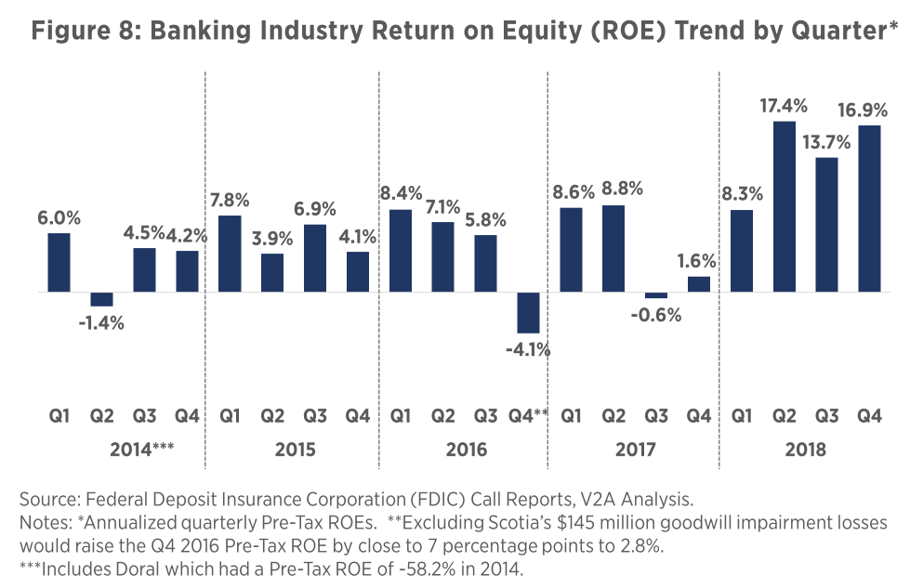

The local banking industry has proved resilient in the aftermath of the hurricanes closing 2018 with a Pre-Tax ROE of 14%, the highest level of profitability since 2005. As illustrated in Figure 8, the industry”s profitability performance was adversely impacted in Q3 and Q4 2017, with a Pre-Tax ROE of -0.6% and 1.6%, respectively, but subsequently returned and surpassed pre-hurricane levels. The financial condition of banks also showed a marked improvement in 2018 with total assets increasing by 5.7%, deposits by 7.9% and its credit portfolio by 2.8%. Loan originations also experienced an uptick in 2018, increasing from $5.9 billion in 2017 to $6.5 billion in 2018, (10%, the first annual increase since 2012). Capital levels have continued to strengthen with an industry level Tier 1 Risk-Based Capital Ratio of 21.7% in 2018, given few opportunities to deploy excess capital. While there were asset quality deterioration concerns in the wake of the hurricanes with the unadjusted nonperforming loans ratio (NPL) exceeding 9%, it has since dropped to 6.8%.

Given the latest trends of most banking profitability levers and economic growth forecasts, we expect a similar or even stronger performance in 2019, unless an unforeseen adverse event materializes. Growth will continue to be a challenge for local banks given the scarcity of inorganic growth opportunities. Organic growth will be contingent upon future economic performance, and while reconstruction efforts will bolster economic activity in the short and medium term, it is less clear which growth drivers will propel the local economy once these funds are expended.

Manufacturing and Related Services

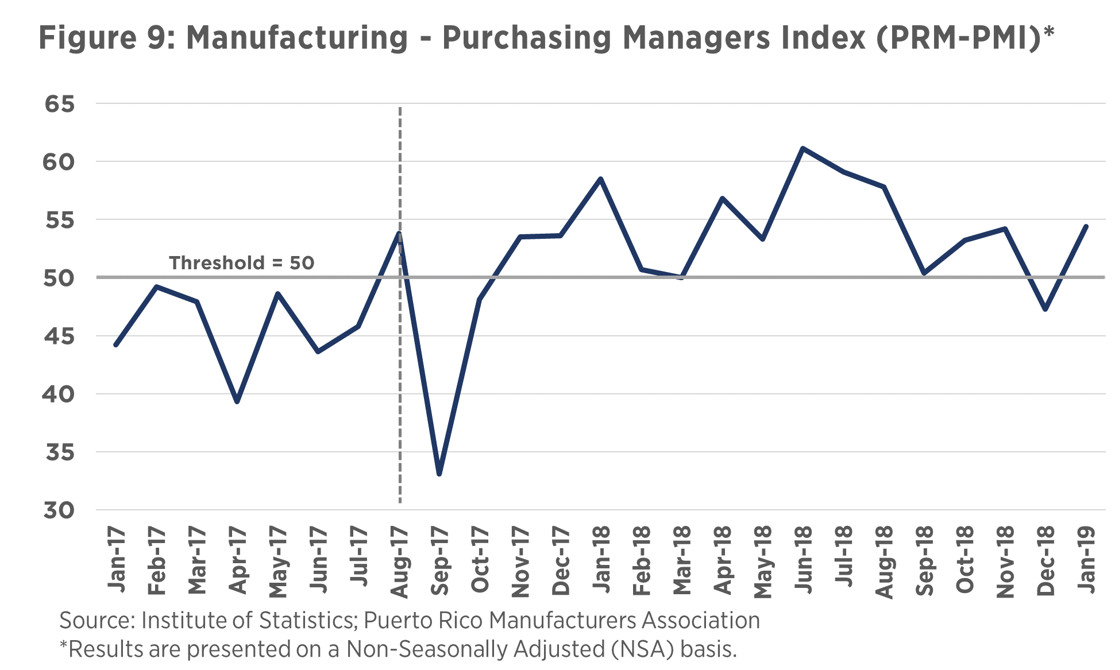

The manufacturing sector of Puerto Rico, which represents roughly half of the Island”s Gross Domestic Product (GDP), 8.3% of total nonfarm employment as of February 2019, and is a core source of revenues for the Government (e.g. Act 154 revenues represented 19% of General Fund Gross Revenues in 2018), was adversely impacted by the hurricanes as seen in Figure 9. The sector”s Purchasing Managers Index (PMI) in September 2017 dipped to its historic low of 33.1. Telecommunications system failure, lack of electricity, and lack or delay of supplies were some of the factors that hindered normal production in the wake of the hurricanes. According to a report by the Institute of Statistics in November 2017, “35% of respondents [to the PMI survey] indicated that they transferred, temporarily or permanently, their supply chain off Puerto Rico partially or completely for some product.”14 Nevertheless, the sector”s robust business continuity plans and supply chain resilience helped minimize losses and recover its industrial capacity.

While hurricane-related disruptions to the Island”s industrial production should not be understated, the largest threat to the sector going forward continues to be the Federal Tax Cuts and Jobs Act (TCJA), passed in Congress in December 2017. It undermines the Island”s tax-based competitive advantage and makes it more attractive to move production to the mainland US since the US corporate tax rate was reduced to 21% from 35%. Furthermore, a 12.5% tax will be levied on intellectual property for Controlled Foreign Corporation (CFC) under this new Federal law. Given the economy”s and government”s reliance on this sector, the impacts of this law in the short-, medium-, and long-term should be closely monitored going forward. The experience of Irma and Maria and potential future hurricanes also put into question the sector”s future growth.

Disaster Relief Funds Update

Community Development Block Grant – Disaster Recovery

The government of Puerto Rico published a Disaster Recovery Action Plan Report which outlines the intended uses for the funds allocated through the Community Development Block Grant – Disaster Recovery (CDBGDR) framework managed by the US Department of Housing and Urban Development (HUD) (see Table 1). The first $1.5 billion (Public Law 115-56/72; Notice 83 FR 5844) were made available by Congress on Feb 1, 2018 and were geared towards housing recovery and activities as seen in the table below. They are to be managed by a joint effort between the PR Department of Housing and the Central Office of Recovery, Reconstruction and Resilience (COR3).

A second allocation of $8.2 billion through the CDBG-DR Program (Public Law 115-123; Notice 83 FR 40314) was made on April 10, 2018. Of this second allocation, $2.8 billion or 33% are allotted to housing programs, including $1.4 billion for home repair, reconstruction, or relocation (see Table 1).

While the importance and need of these allocated funds cannot be overstated, it falls short of the $94.4 billion requested by the local government to Congress to address the unmet needs established in the Build Back Better report.15 A study found that “nearly half of all FEMA disaster relief is explained by political influence rather than actual need”.16 Given Puerto Rico”s limited leverage in Congress due to its political condition as an unincorporated territory of the US subject to the Territorial Clause of the US Constitution, acquiring the funds necessary to adequately address its needs will be a challenge. Another challenge has been the pace of disbursements of these much-needed funds given onerous bureaucratic hurdles.

Disparities in US Federal Response

A report by BMJ Global Health quantified inequities in US Federal response to hurricane disasters in Texas, Florida, and Puerto Rico finding that the “Federal response was faster and more generous across measures of money and staffing to Hurricanes Harvey and Irma in Texas and Florida, compared with Hurricane Maria in Puerto Rico” despite Maria causing more damage.17 The study looks at Federal response 6 months after landfall. Nine days after landfall, Harvey and Irma survivors received $100 million, while Maria survivors received $6 million in aid. Within the first 2 months, Harvey and Irma survivors received $1 billion. It took double the amount of time, 4 months, for Maria survivors to receive that amount.

When it comes to staffing levels, the study also found significant disparities between Hurricanes Harvey and Irma in Texas and Florida vis-à-vis Hurricane Maria in Puerto Rico. After nine days from landfall, Texas received 30,000 Federal employees, Florida received 19,000, and Puerto Rico received 10,000. The peak level of Federal employees for Puerto Rico was 19,000, one month after landfall, while the peak for Texas was 31,000. The study also notes disparities when it comes to delivery and timing of Federally appropriated funds, amount of food, water, tarps, and helicopters.

Post-Disaster Federal Contracting and Procurement

An analysis of post-hurricane Federal contracting and procurement can help see to what extent local firms are being hired, to what extent the local economy will benefit, what sectors will be most impacted by these contracts, and how does the Federal response compare to other comparable jurisdictions. The Center for a New Economy (CNE) published a report18 tracking post-hurricane Federal contracting in Puerto Rico, finding that as of August 22, 2018 (336 days post-landfall), $5 billion have been obligated for Federal work in Puerto Rico, $4.3 billion or 89.7% going to firms based in the US mainland and $490 million or 10.3% going to Puerto Rico. The majority of these contracts (91%) have been obligated by the US Department of the Army, which includes the US Army Corps of Engineers, and the Federal Emergency Management Agency (FEMA). When examining Federal contracting by sector, they found that the bulk of it is going to construction work. In the Fiscal Plan for Puerto Rico (September 7, 2018 revision) it is stated that “in assessing impact of disaster relief funding on the economy of Puerto Rico, it is important to isolate what portion of the disaster relief funding directly affects the local economy and what portion flows to entities off-Island. The Fiscal Plan estimates that, on a weighted average basis, 12.5% of funds will directly impact the local economy.”19 This is very much in line with CNE”s findings. Furthermore, the study also pointed out that Puerto Rico firms have been conducting lower value-added activities than US mainland firms.

The study also compared Federal reconstruction expenditures and activities in post-Katrina Louisiana and post-Maria Puerto Rico. The Federal contracting and procurement spending in Louisiana in the first 336 days post-landfall was $12 billion, more than twice the amount spent in Federal contracts in Puerto Rico. Similar to the case of Puerto Rico, 89% went to off-state contractors, while 11% went to Louisiana-based firms.

Concluding Remarks

The historic size, magnitude, and impact of Hurricanes Irma and Maria on Puerto Rico needed to be met with a proportional response. The latest trends and developments seem to suggest that the response has fallen short of expectations and needs. Prior to the hurricanes, the Island was already facing an economic, fiscal, debt, and demographic crisis dating back to more than a decade ago.

The Government of Puerto Rico, in its recently submitted revised Fiscal Plan (March 10, 2019)20, outlines the reforms it is betting on to kickstart the economy including human capital and welfare reform, ease of doing business reform and power sector reform. Fiscal measures seeking to establish fiscal discipline and stewardship going forward are also a big part of the plan. The net results of these reforms and measures are still to be seen. While the plan projects that the economy will grow modestly from FY2019 to FY2023 (4.1%, 3.8%, 1.5%, 3.5%, 1.5%, respectively), buttressed by disaster relief funds, it forecasts stagnation in FY2024 and beyond.

On a more promising note, many are banking on Opportunity Zones created by the Federal Tax Cuts and Jobs Act of 2017, which provide substantial tax benefits to investors, as a potential important source of investment, especially when considering that 95% of the Island qualifies.21 Nevertheless, while Puerto Rico will see Federal disaster dollars at work in the short- and medium-term, much uncertainty remains about its long-term prospects.

Endnotes and References

1. The Economic Activity Index (EAI) of Puerto Rico published by the Economic Development Bank (EDB) for Puerto Rico, alongside other key monthly economic indicators, are available at https://www.bde.pr.gov/BDESite/PRED.html

2. Labor market indicators for Puerto Rico are available at the US Bureau of Labor Statistics” website https://www.bls.gov/eag/eag.pr.htm and the Department of Labor and Human Resources of Puerto Rico http://www.mercadolaboral.pr.gov/.

3. A Report by the Center for Puerto Rican Studies published on June 2018 titled The Housing Crisis in Puerto Rico and the Impact of Hurricane Maria, provides a more detailed analysis of the challenges faced by Puerto Rico”s housing market prior to and following the hurricanes. Available at https://centropr.hunter.cuny.edu/sites/default/files/data_briefs/HousingPuertoRico.pdf

4. Puerto Rico Disaster Recovery Action Plan: For the use of CDBG-DR funds in response to 2017 Hurricanes Irma and Maria, available at http://www.cdbg-dr.pr.gov/wp-content/uploads/2019/03/111618_PRDOH-Action-Plan_SubstantialAmendment_030819_Approved.pdf

5. The size of the tourism sector has been traditionally calculated by dividing total visitors” expenditures found in Table 19 of the Planning Board”s Statistical Appendix (i.e. for FY2017 $4.09 billion in visitors” expenditures/$70.57 billion Gross Product). Foundation for Puerto Rico (FPR) and other stakeholders have called for the development of a tourism satellite account (TSA) and a National System of Tourism Statistics (NSTS) for Puerto Rico to strengthen the island”s tourism statistics infrastructure. See FPR”s report titled La Economía del Visitante: hacia un sistema nacional de estadísticas de turismo available at https://www.foundationforpuertorico.org/july17/.

6. World Travel & Tourism Council (April 2018) The Impact of the 2017 Hurricane Season on the Caribbean”s Tourism Sector, available at https://www.wttc.org/-/media/files/reports/2018/caribbean-recovery-report—executive-summary.pdf

7. V2A Insight: From emerging to mainstream: internet platforms Airbnb and HomeAway are transforming the Puerto Rico lodging infrastructure, available at http://www.v2aconsulting.com/news-detail/128-126-from-emerging-tomainstream-internet-platforms-airbnb-and-homeaway-aretransforming-the-puerto-rico-lodging-infrastructure/

8. V2A Insight titled Tourists are increasingly choosing cruise ships and short-term rentals to visit Puerto Rico provides a deeper discussion on post-hurricane tourism activity. Available at http://www.v2aconsulting.com/news-detail/128-122-tourists-are-increasingly-choosing-cruise-ships-andshort-term-rentals-to-visit-puerto-rico/

9. See Discover Puerto Rico”s website at https://www.puertoricodmo.com/DMOLanding/

10. See The Wall Street Journal article titled A Year After Maria, Puerto Rico Is Pushed to Precipice, available at https://www.wsj.com/articles/a-year-after-maria-puertorico-is-pushed-to-precipice-1537435802

11. See V2A”s Puerto Rico Banking Industry Report – Issue XXXIX January to December 2018, available at http://www.v2aconsulting.com/news-detail/72-128-pr-banking-industry-report-q4-2018/

12. See V2A Insight titled Popular becomes the indisputable leader of the auto financing industry with the acquisition of Reliable, available at http://www.v2aconsulting.com/news-detail/128-113-popular-becomes-the-indisputable-leader-of-the-autofinancing-industry-with-the-acquisition-of-reliable/

13. See Caribbean Business article titled Economist Provides Status of Puerto Rico Economy at Auto Industry Seminar available at https://caribbeanbusiness.com/economist-providesstatus-of-p-r-economy-at-auto-industry-seminar/

14. The Puerto Rico Manufacturing Purchasing Managers Index (PRM-PMI) measures short-run business conditions in Puerto Ricos manufacturing sector and is calculated as the simple average of 5 sub-indexes, representing different business conditions in manufacturing establishments: New Orders PMI, Production PMI, Employment PMI, Supplier Deliveries PMI, Own Inventories PMI. A PMI above 50 represents an expansion when compared with the previous month, a PMI under 50 represents a contraction, and a reading at 50 indicates no change.

15. Build Back Better Report: Request for Federal Assistance for Disaster Recovery published on November 2017, available at https://media.noticel.com/o2com-noti-media-us-east-1/document_dev/2017/11/13/Build%20back%20better%20Puerto%20Rico_1510595877623_9313474_ver1.0.pdf

16. Garrett, T. A., & Sobel, R. S. (2003). The political economy of FEMA disaster payments. Economic inquiry, 41(3), 496-509.

17. Willison, C. E., Singer, P. M., Creary, M. S., & Greer, S. L. (2019). Quantifying inequities in US Federal response to hurricane disaster in Texas and Florida compared with Puerto Rico. BMJ Global Health, 4(1), e001191. Available at https://gh.bmj.com/content/4/1/e001191

18. Center for New Economy published a report titled Transforming the Recovery into Locally-led Growth: Federal Contracting in the Post-Disaster Period which examines Federal post disaster contracting. Available at http://grupocne.org/2018/09/26/transforming-the-recovery-into-locally-ledgrowth-Federal-contracting-in-the-post-disaster-period/

19. Fiscal Plan for Puerto Rico: As submitted to the Financial Oversight and Management Board for Puerto Rico (September 7, 2018 Revision) available at http://www.aafaf.pr.gov/assets/pr-fiscal-plan-090718.pdf

20. Revised Fiscal Plan for Puerto Rico: As submitted to the Financial Oversight and Management Board for Puerto Rico (March 10, 2019) available at http://www.aafaf.pr.gov/assets/fiscal-plan-pr-fy2020-draft-03-10-2019.pdf

21. Ernst & Young report titled Puerto Ricos Governor proposes tax incentives bill for Opportunity Zones published on February 5, 2019, available at https://www.ey.com/Publication/vwLUAssets/Puerto_Ricos_Governor_proposes_tax_incentives_for_Opportunity_Zones/$FILE/2019G_000327-19Gbl_PR%20-%20Tax%20incentives%20for%20Opportunity%20Zones.pdf

The “Puerto Rico Post-2017 Hurricane Season: Latest Trends & Developments” is the third of a series of special V2A publications given the extraordinary exogenous shock impacting Puerto Rico”s economy.

V2A”s first special post-hurricane issue, the “Puerto Rico Post-2017 Hurricane Season: Initial Insights & Outlook”, is available here.

V2A”s second special post-hurricane issue, the “Puerto Rico Post-2017 Hurricane Season: Update & Revised Outlook”, is available here.

V2A”s quarterly publication, the “PUERTO RICO BANKING INDUSTRY REPORT”, is available here.

V2A contributors to this special V2A publication:

Olivier Perrinjaquet

Disclaimer

Accuracy and Currency of Information: Information throughout this report is obtained from sources which we believe are reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. While the information is considered to be true and correct at the date of publication, changes in circumstances after the time of publication may impact the accuracy of the information. The information may change without notice and V2A is not in any way liable for the accuracy of any information printed and stored, or in any way interpreted and used by a user.